New Updates

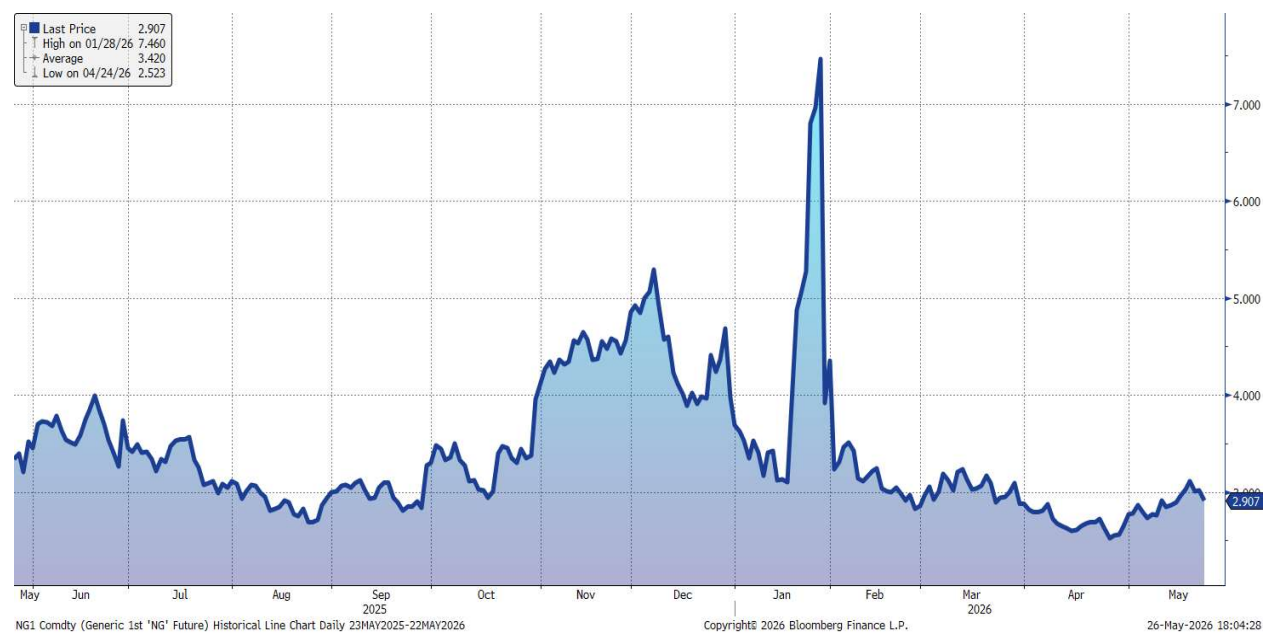

FUEL HEDGING & NATURAL GAS MARKET UPDATE (May 25, 2026)

PRICES LOWER – INVENTORIES HIGHER VS. FIVE-YEAR AVERAGE AND HIGHER VS. EXPECTATIONS – PRODUCTION LOWER – DEMAND HIGHER – EXPORTS LOWER – RIG COUNT LOWER – HEDGE FAVORABILITY HIGHER

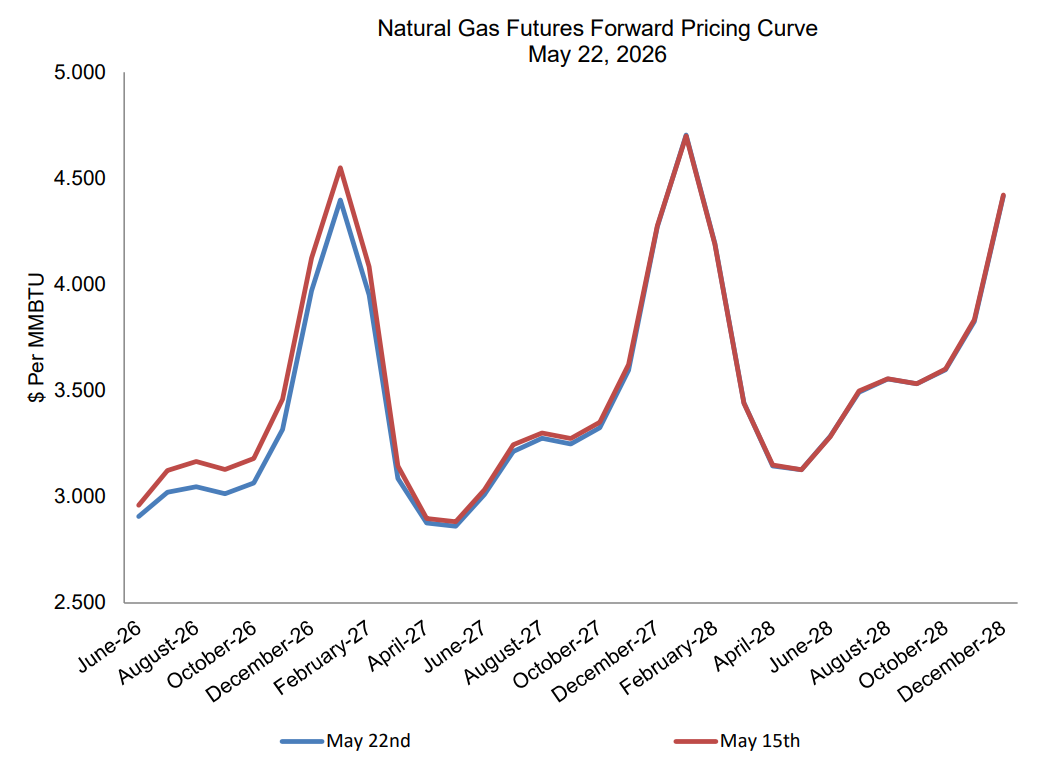

Price Movement:

- Spot price decreased by $0.053 per MMBTU

- Forward price decreased by $0.005 per MMBTU

Key Drivers:

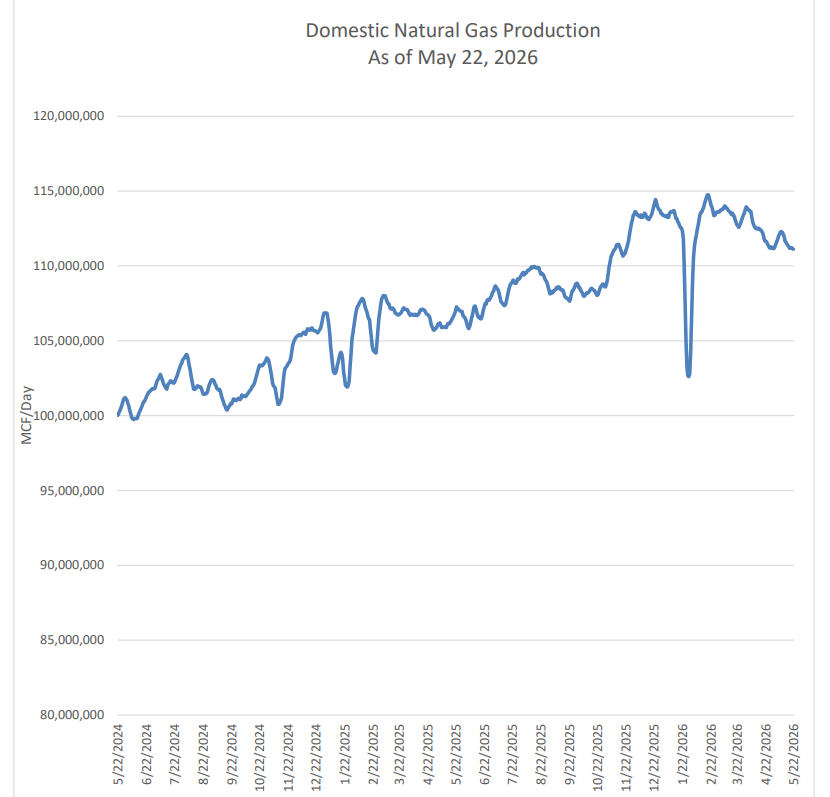

- Production: Domestic production decreased by 373,735 Mcf per day to 111,121,347 Mcf per day (-0.34%), supporting prices.

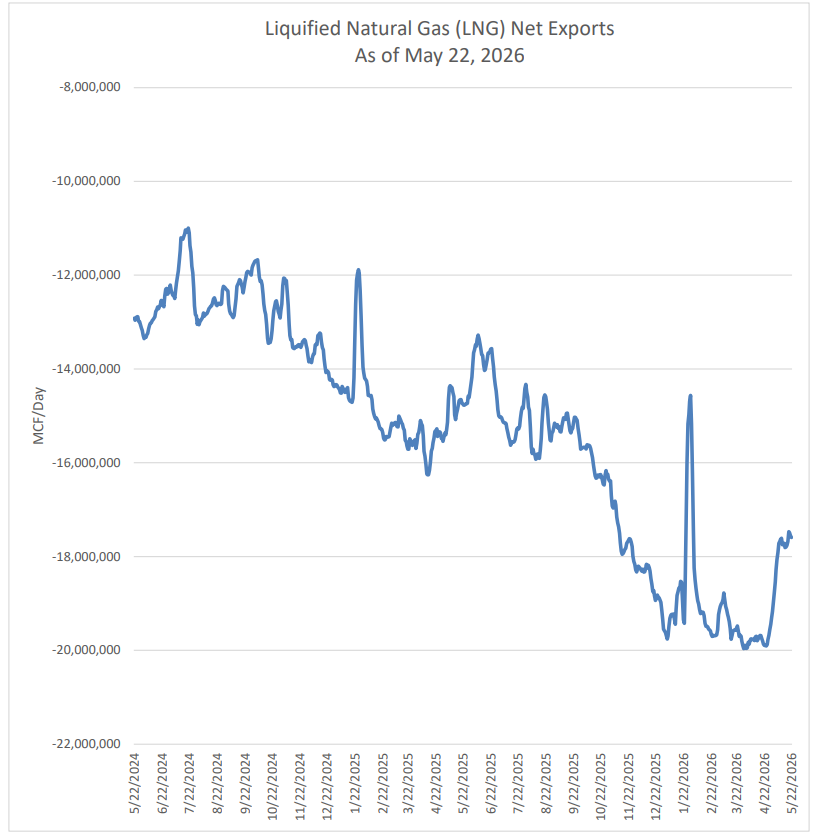

- LNG Exports: Freeport LNG terminal exports decreased by 1.21% from the previous week, which is negative for prices, though still 38.73% above the five-year average.

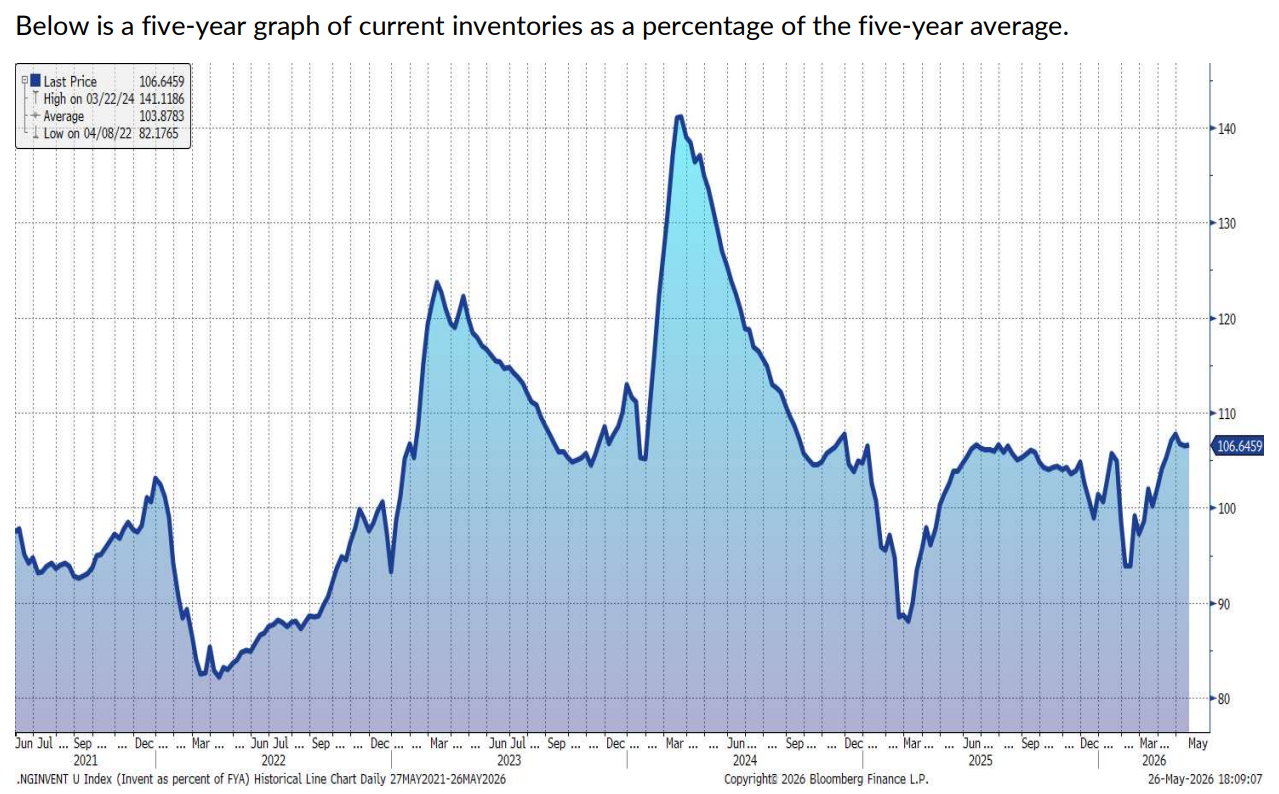

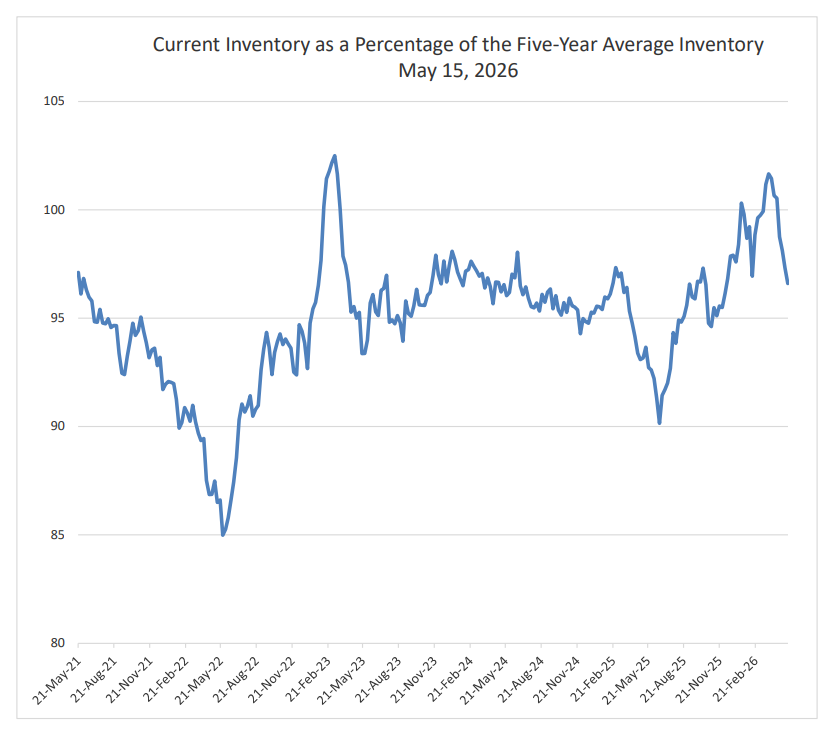

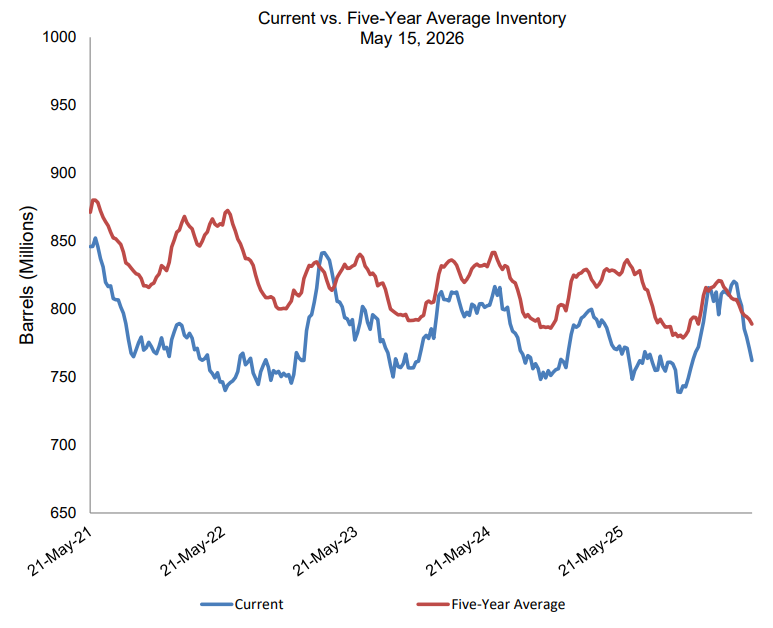

- Inventories: Total natural gas inventories increased by 101 Bcf, higher than expectations (+5 Bcf) and the five-year average (+9 Bcf), signaling pressure on prices.

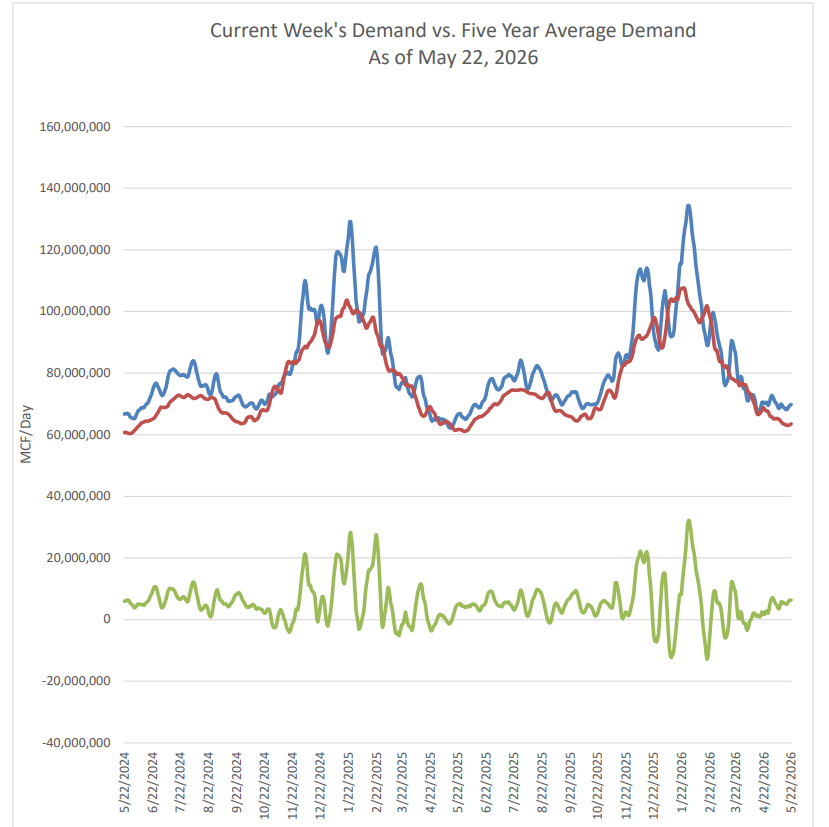

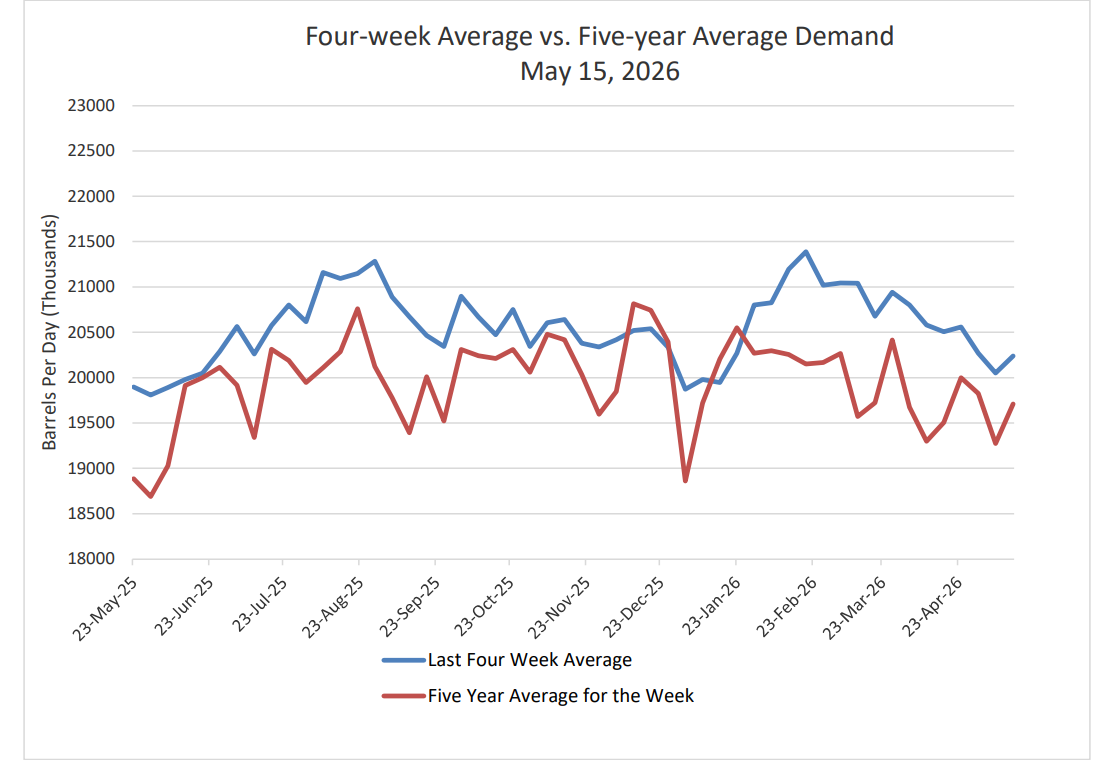

- Demand: US domestic natural gas demand increased by 1.79% week over week and is +10% above the five-year average, supporting prices.

- Rig Count: Decreased by 3 rigs to 125, which is positive for prices.

Market Indicators:

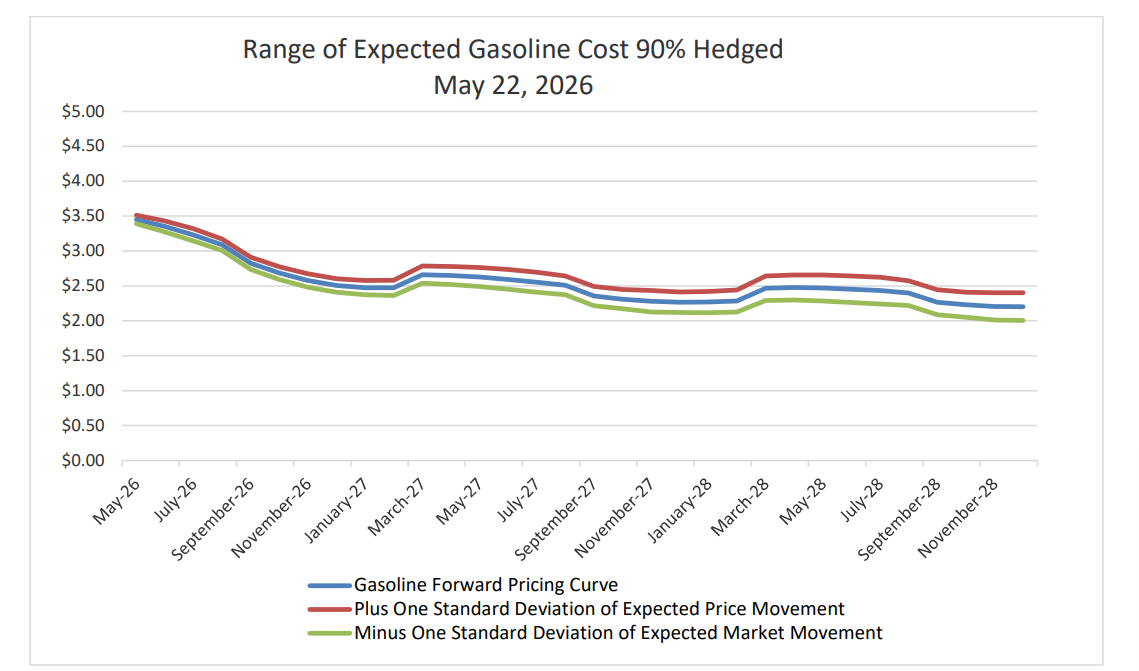

- Hedge Favorability Index: Increased to 24.50%, indicating more attractive conditions for 1–3 year hedging.

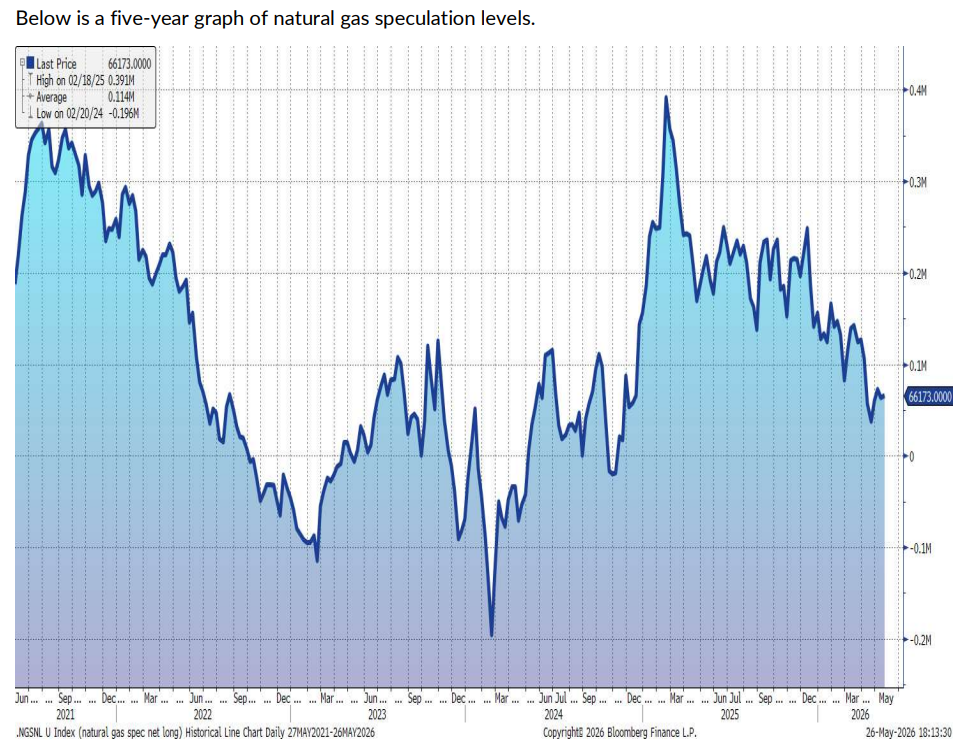

- Speculation: Net speculative long positions increased by 27,695,000 MMBTU to 661,730,000 MMBTU (27.68% of current inventory), which is mixed for price signals.

Forecast:

Natural gas prices remain mixed. Higher inventories and decreased LNG exports weigh on prices, while lower production and rig count, coupled with rising demand, provide stability in the market.

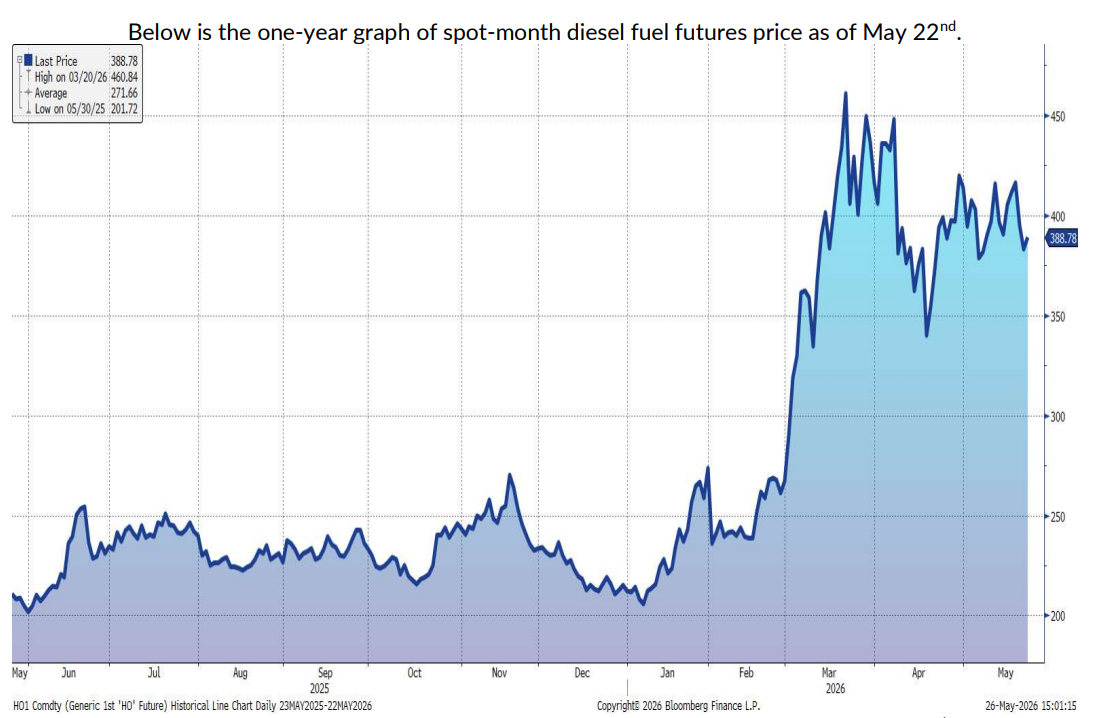

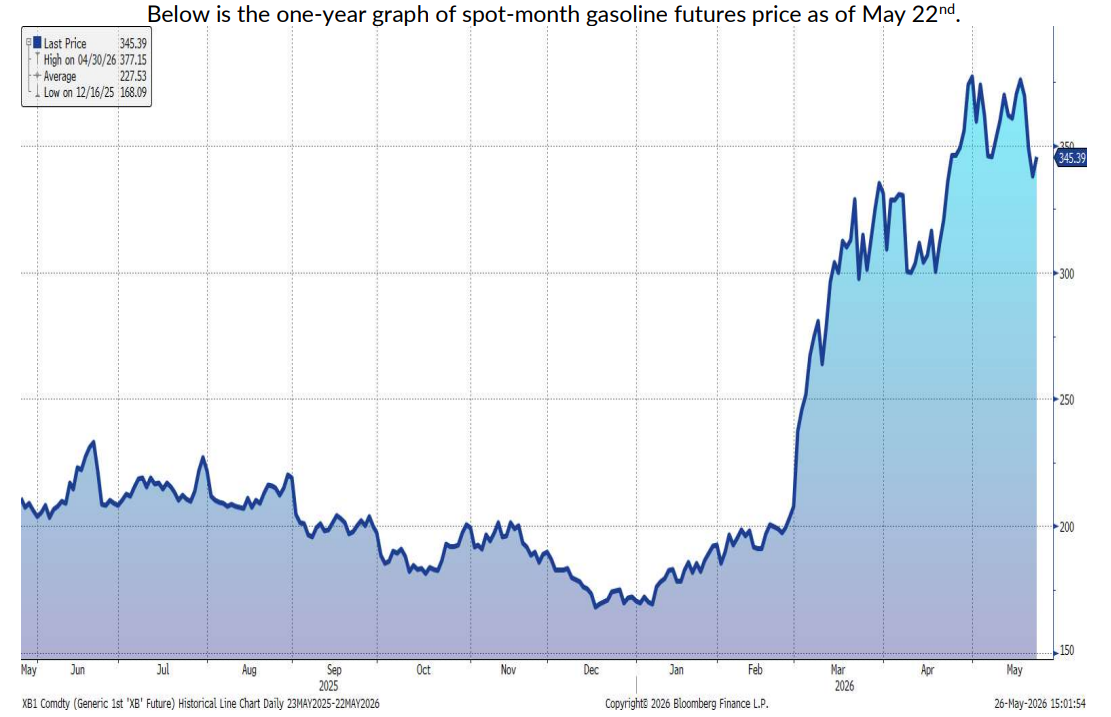

FUEL HEDGING & PETROLEUM MARKET COMMENTARY (May 25, 2026)

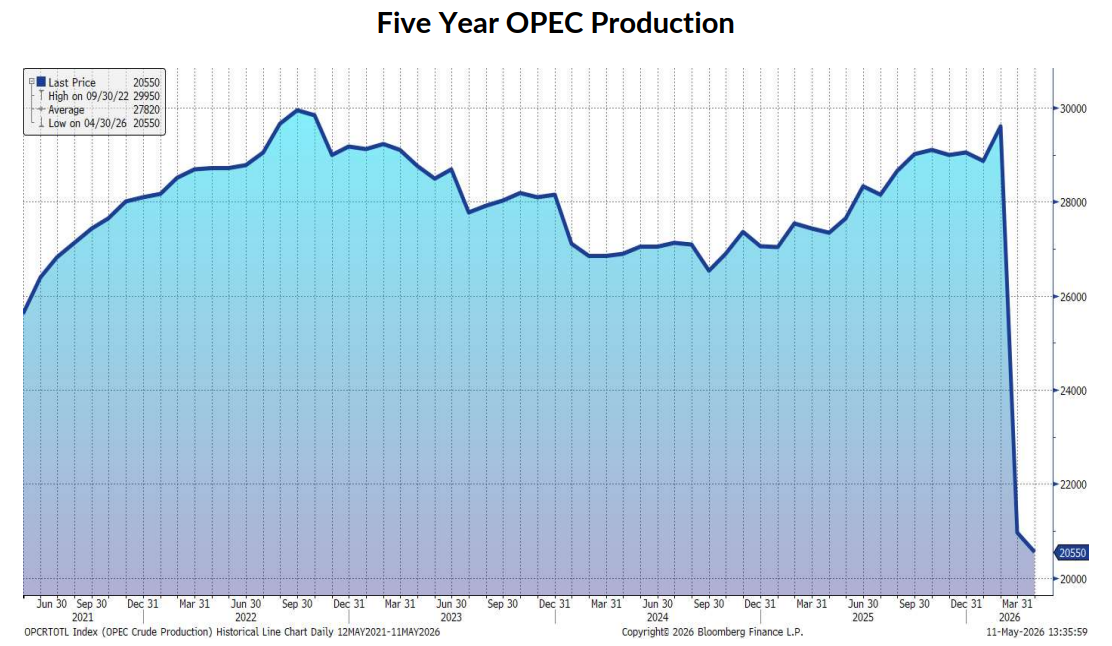

PRICES MIXED – CRUDE OIL PRODUCTION LOWER – INVENTORY LOWER – DOLLAR LOWER – STOCK MARKET HIGHER – SPECULATION HIGHER – DEMAND HIGHER – HEDGE FAVORABILITY LOWER – EXPECTED PRICE VARIABILITY/CASH FLOW AT RISK MIXED

Price Movement:

- Diesel: Spot -$0.1656 per gallon, Forward +$0.0230 per gallon

- Gasoline: Spot -$0.2480 per gallon, Forward -$0.0070 per gallon

Key Drivers:

- Iran Conflict: Risk remains from ongoing US-Iran tensions; partial military actions and “dark transits” support supply and negatively affect prices.

- Strait of Hormuz: Remains largely closed, restricting overall supply, supporting prices.

- Global Inventories: Drawdowns continue at record pace, positive for prices.

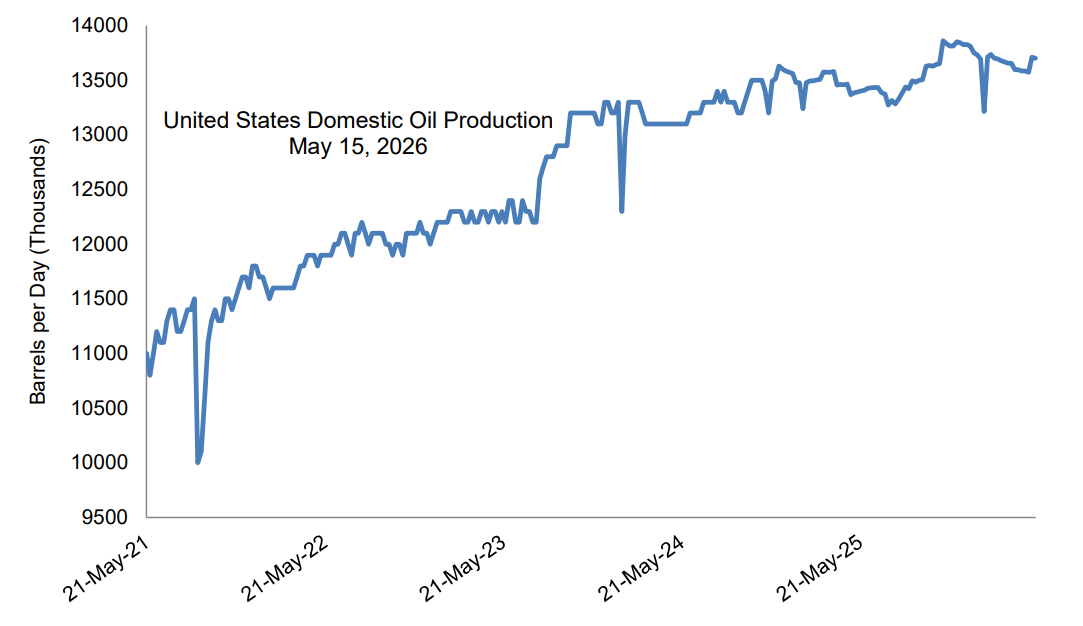

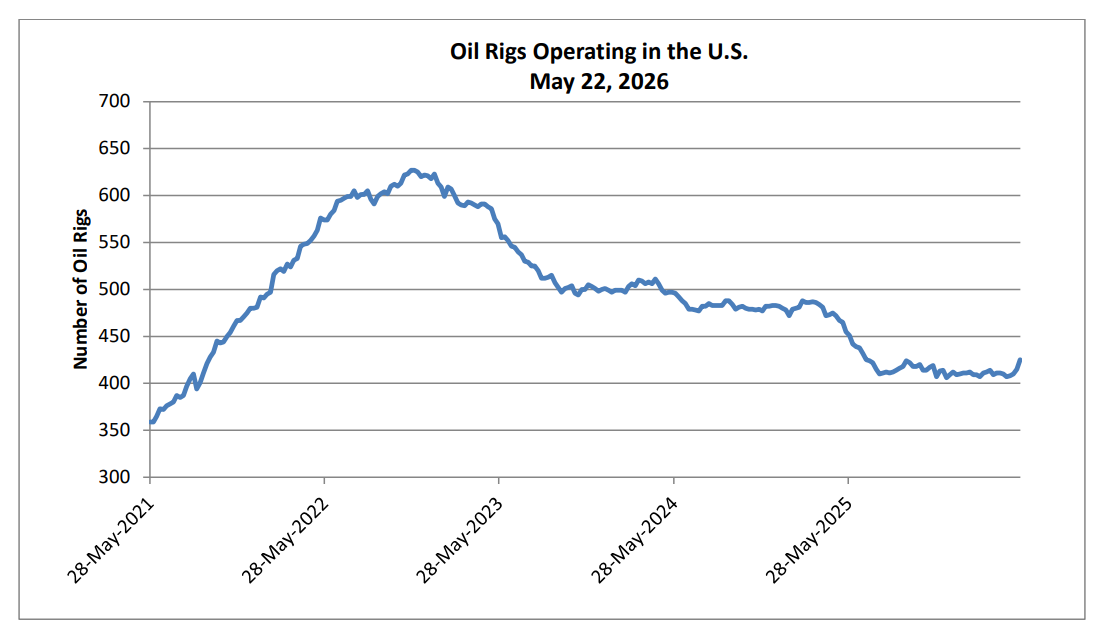

- US Production & Drilling: Domestic production is slightly higher over the past two weeks; oil rig activity increased by 10 rigs, which can offset price gains.

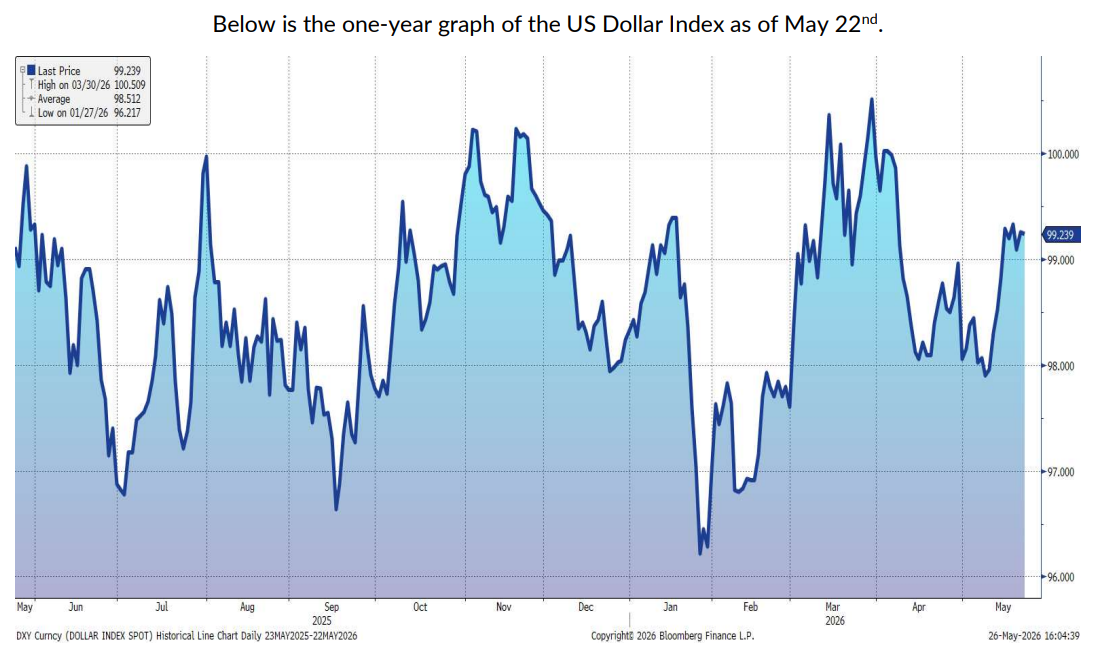

- US Dollar: Lower, which is positive for petroleum prices.

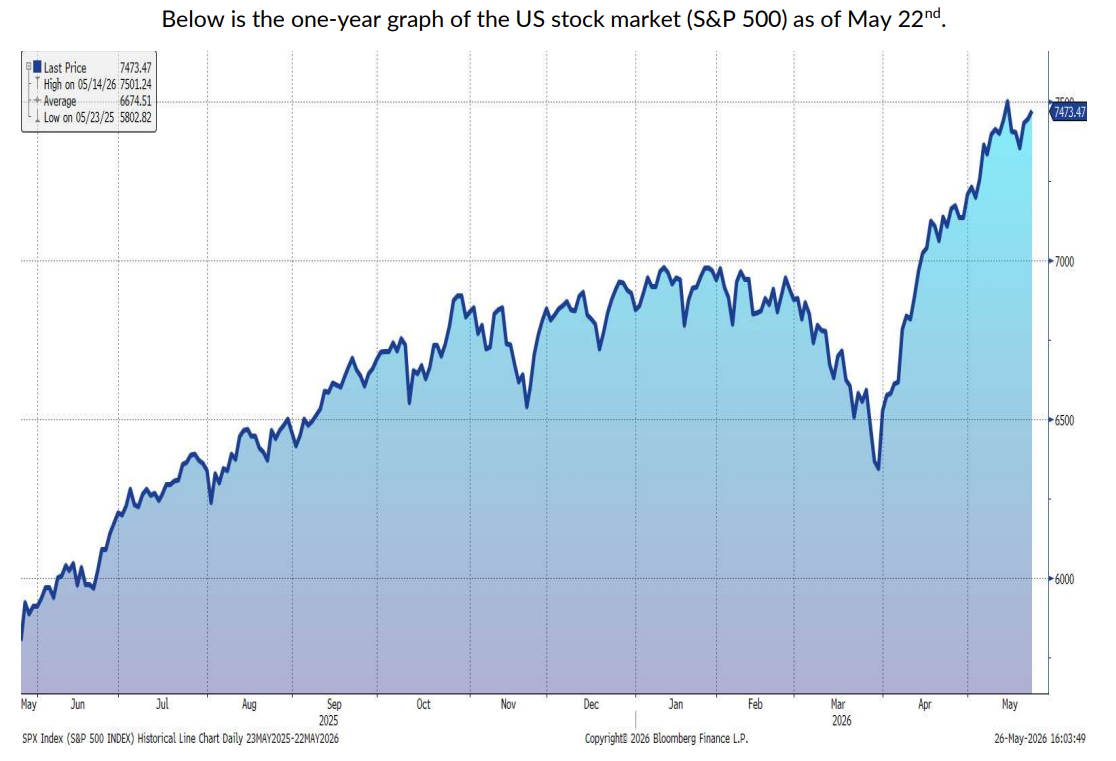

- Stock Market: Higher, supporting petroleum demand expectations.

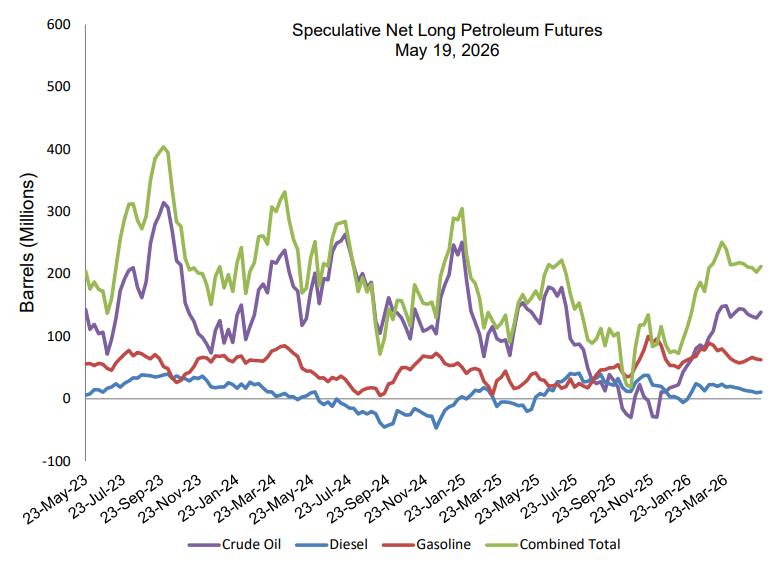

- Speculation: Net speculative long positions increased by 9.26 million barrels to 212.2 million barrels (27.84% of inventories), mixed for prices.

- Domestic Demand: Weekly petroleum demand increased by 2.81% vs. previous week, supporting prices.

Forecast:

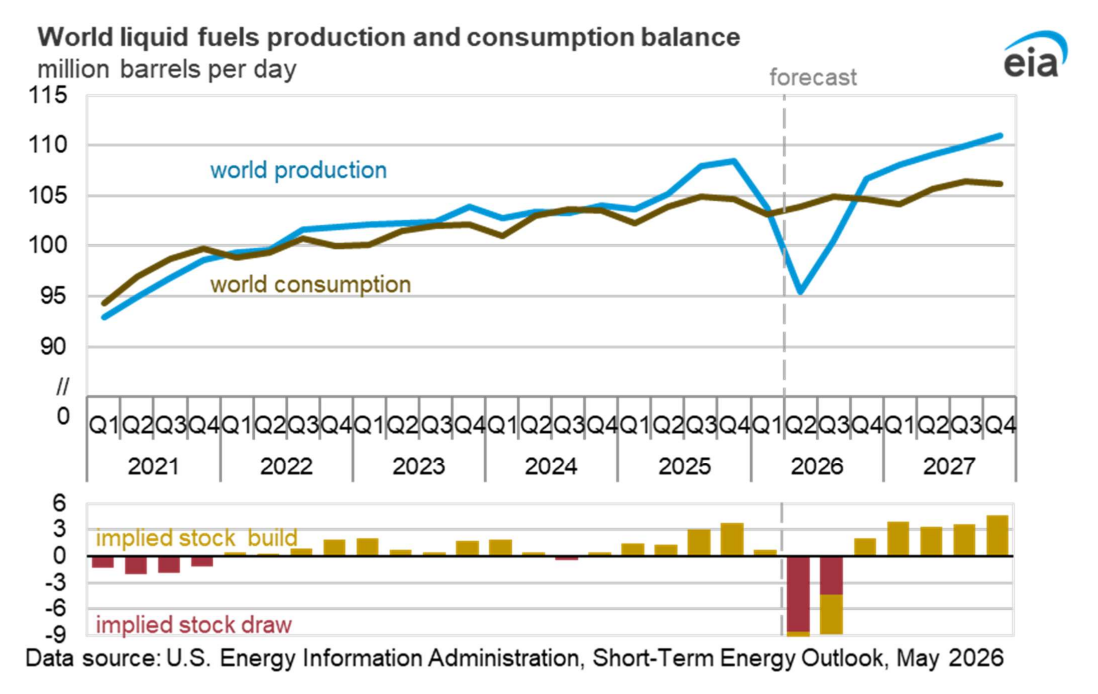

Petroleum prices are likely to remain volatile due to geopolitical tensions, ongoing supply restrictions, inventory fluctuations, and speculation levels. The May 2026 Energy Department forecast shows a larger global deficit for 2026, with surplus expected in 2027, supporting higher prices for the remainder of 2026.